Cryptocurrencies operate on decentralized networks but face diverse legal frameworks worldwide. Ensuring Web3 legal compliance means understanding each country’s approach: some nations welcome crypto, while others ban or restrict it.

The EU’s Markets in Crypto-Assets (MiCA) regulation is a first-of-its-kind unified framework (effective 2024–2025) requiring all crypto firms to be licensed and to collect sender/ recipient data on transfers. Other jurisdictions have different rules – the UK, Singapore and Japan already have dedicated crypto licensing schemes, whereas China and others impose outright bans. This global patchwork means founders must tailor their compliance programs to each market and monitor evolving international crypto law closely.

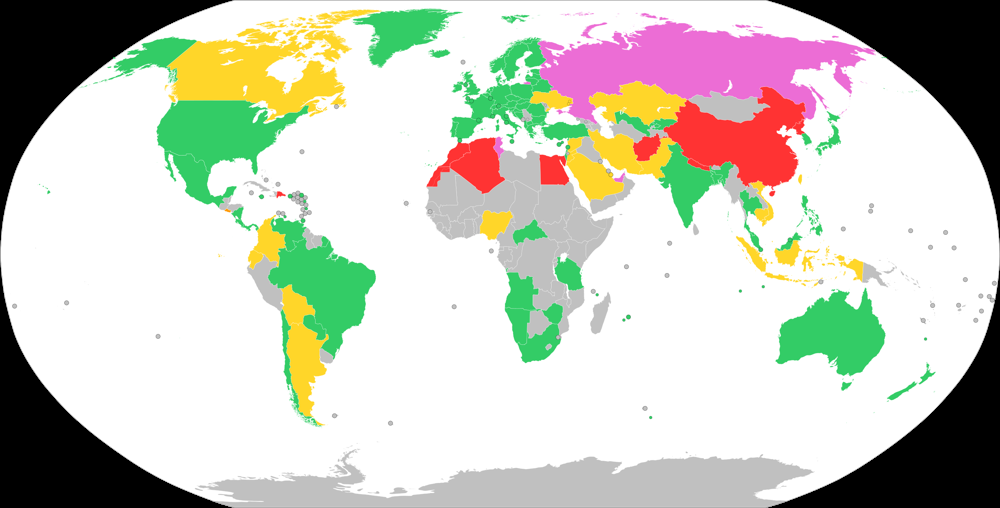

Figure: Global legal status of Bitcoin (green = allowed, red = banned). Crypto regulations vary widely. The EU’s MiCA regime (May 2023) is the first comprehensive crypto law, demanding licenses for any issuer or exchange and strict AML/KYC measures.

Other “crypto-friendly” countries (e.g. UK, Singapore, Japan) have clear crypto licensing rules, helping to protect consumers. By contrast, some countries still prohibit exchanges and mining (as seen in red), forcing businesses to avoid those markets. In practice, firms must map out compliance for each region – tracking FATF guidelines, local tax rules, data privacy laws, and any new legislation – to offer crypto services globally without legal risk.

KYC/AML Obligations and Implementation

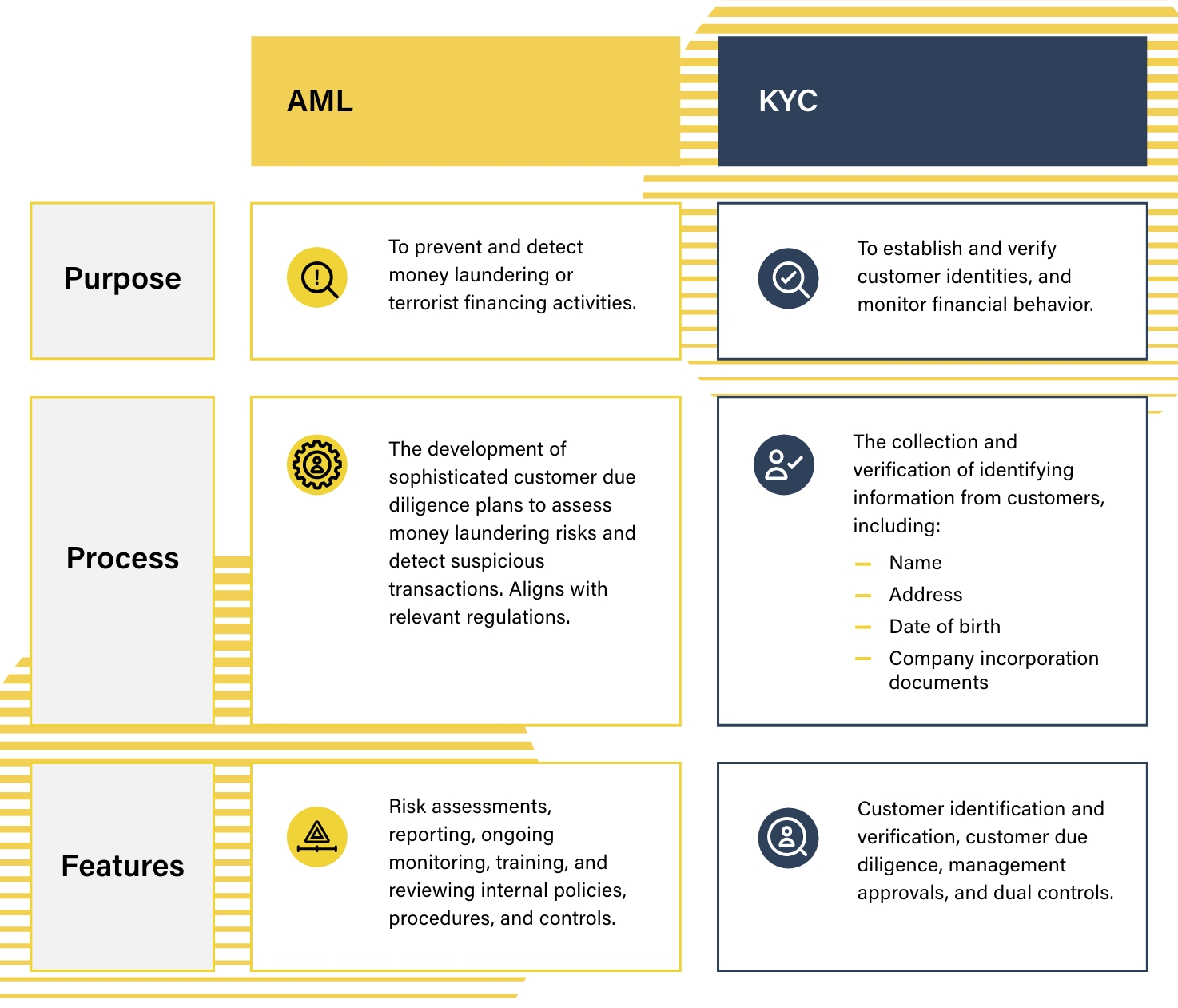

Robust KYC/AML programs are foundational. Exchanges and wallets must verify customer identities and monitor transactions for money laundering, terrorism financing, fraud and other illicit activity.

For example, crypto firms are generally treated like banks: in the U.S. they are Money Services Businesses under FinCEN, so the Bank Secrecy Act applies. This means collecting identifying information (name, DOB, address, ID documents) at onboarding, screening against sanction lists, and running a risk-based transaction monitoring system.

Compliance experts warn that one-size-fits-all controls are risky, companies should customize monitoring for their business and set alerts tuned to local threats. Failure to enforce KYC/AML can be costly: Coinbase agreed to pay $50M (plus $50M to improve its systems) after New York regulators found major AML/KYC gaps in its program.

In short, implement automated KYC verification and ongoing AML screening as core parts of your compliance strategy.

AML and KYC: Ensuring Compliance and Combating Financial Crimes (Source: ComplyAdvantage)

Licensing Strategies for Cross-Border Crypto Operations

A multi-pronged licensing strategy is essential. In practice, many crypto firms obtain multiple registrations or licenses to cover key markets. For example, a U.S. exchange typically registers with FinCEN and secures money-transmitter licenses in the states where it operates. It may then obtain formal crypto licenses elsewhere – for example, Coinbase recently acquired FCA-issued VASP registration in the UK to offer services legally.

In the EU, prepare to apply for MiCA authorization (acting like an electronic-money or investment firm license), which should grant pan-European compliance under one rulebook. Other options include partnering or operating through entities in crypto-friendly jurisdictions (e.g. Swiss FINMA license, Dubai’s Virtual Assets regulator, or Australia’s Digital Currency Exchange license). In all cases, each country’s unique international crypto law must be met – a global analysis firm notes that “each country will often have its own rules relating to KYC protocols and crypto taxation,” so failing to comply can lead to bans or fines.

- United States: Register as an MSB with FinCEN and obtain money-transmitter licenses by state.

- European Union: Seek MiCA crypto-asset service provider authorization (a unified framework effective in 2024–2025).

- United Kingdom: Complete FCA VASP registration (as Coinbase did in 2025) and satisfy UK AML regulations.

- Asia-Pacific: Fulfill local requirements (e.g. MAS license in Singapore, FSA registration in Japan, local crypto laws in Korea/Japan).

- Other Hubs: Consider Switzerland, Dubai, or other innovation zones for easier entry, but always verify their specific licensing rules.

Case Study

Even major exchanges have learned compliance the hard way. Binance faced regulatory crackdowns worldwide: Italy’s Consob declared it “not authorised” in 2021, and the UK’s FCA barred it from regulated activities. These actions shut Binance out of those markets despite its global brand, a clear lesson that ignoring local licensing has consequences.

Coinbase, by contrast, has actively sought regulatory approval, it obtained UK registration. Yet Coinbase still paid a $100M penalty (with an additional $50M investment in compliance) after New York found serious gaps in its KYC/CDD and monitoring systems.

The takeaway: no one is exempt. Regulators treat crypto firms like banks – weak controls lead to enforcement. In practice, businesses must invest in compliance infrastructure (staff training, audit, compliance tech) from day one to avoid repeating these pitfalls.

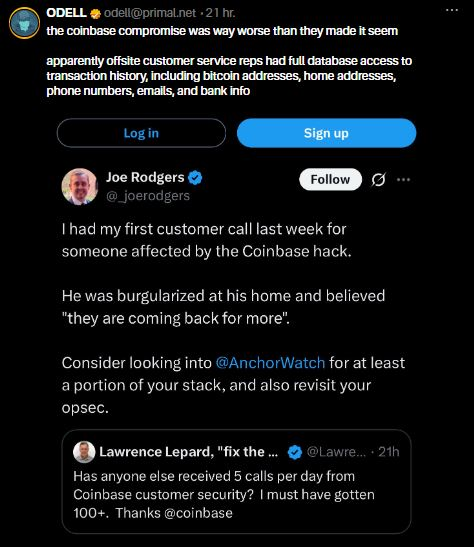

User testimonies on Twitter/X reveal the real-world consequences of poor data security. In the aftermath of the Coinbase incident, one user reported a home burglary potentially linked to leaked customer information – a stark reminder that compliance must include robust KYC/AML and data protection systems. (Source: X)

Common Pitfalls and Best Practices

Pitfalls to avoid:

- Skipping Local Licenses: Launching without required approvals can get you shut down (as with Binance). Always verify and obtain necessary registrations or licenses in each jurisdiction.

- Weak KYC/AML Processes: Inadequate customer due diligence will attract fines (see Coinbase’s $100M penalty for AML lapses). Don’t rely on manual checks alone, use automated identity verification and sanctions screening.

- Inconsistent Controls: Failing to customize AML monitoring is a mistake. Maintain tailored, risk-based alerts for transactions so that regulatory changes or new schemes are caught quickly.

- Ignoring Travel Rule: As of 2024–26, many regions require the FATF “travel rule” (passing sender/receiver info). Failing to implement it end-to-end can lead to non-compliance.

- Outdated Policies: Crypto law evolves fast. Continuously update your policies and systems (e.g. by monitoring emerging laws like MiCA or new guidance) to avoid falling out of step.

- Data and Tax Compliance: Don’t overlook data protection (e.g. GDPR) and crypto taxation rules in each country. These often accompany licensing regimes.

Best practices

Build a global compliance framework that is flexible. Common strategies include: hiring experienced compliance officers, running regular internal audits, using blockchain analytics tools, and consulting local legal experts. Make compliance a shared responsibility across the organization.

Always document your KYC/AML procedures and revisit them when entering a new market. Engaging proactively with regulators (rather than reactively) can also smooth market entry. Overall, aligning with FATF standards and high-rated jurisdictions’ regulations will help create a scalable compliance posture.

Conclusion: Partnering for Compliance

Navigating cross-border crypto compliance is complex but manageable with the right plan. By analyzing each jurisdiction’s requirements (from KYC/AML checks to licensing thresholds) and learning from industry examples, blockchain businesses can expand globally without legal entanglements.

Twendee Labs specializes in blockchain development and regulatory strategy, we help projects implement robust compliance solutions across multiple regions. Compliance is an ongoing journey, with expert partners like Twendee, your crypto venture can grow worldwide while staying on the right side of the law.

To explore how Twendee helps companies make AI work from the inside out, visit our site, connect on LinkedIn, or follow us on Twitter/X.