In enterprise finance, the most consequential shifts rarely arrive as flashy new products. They emerge quietly, at the infrastructure layer, where reliability, integration, and control matter more than user-facing novelty. Stablecoins are now following this path. What began as a crypto-native alternative for trading and remittances is increasingly being repositioned as a stablecoin payment infrastructure that underpins enterprise payments, rather than a feature added on top of existing systems.

This transition reflects a broader realization across finance and technology leadership. Payments are no longer judged solely by speed or cost. They are evaluated by how well they integrate with core financial systems, how predictably they settle, and how defensible they are under audit and regulatory scrutiny. In this context, stablecoins are less interesting as “digital dollars” and far more important as a programmable settlement layer that can be embedded directly into financial infrastructure.

Stablecoin payment infrastructure as the settlement layer

For decades, enterprise payments have been built on layered intermediaries. Payment initiation, clearing, settlement, reconciliation, and reporting are handled by different systems, often across different institutions and jurisdictions. This fragmentation is especially visible in cross-border payments, where settlement can take days, liquidity is trapped in correspondent accounts, and reconciliation becomes a manual, error-prone process.

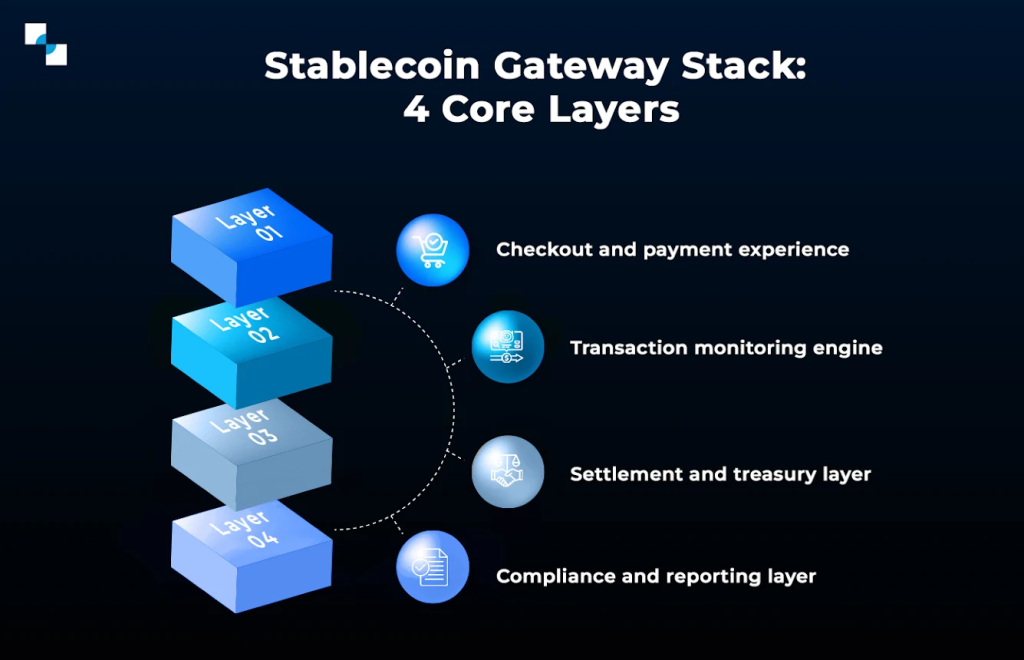

Stablecoin payment infrastructure layered stack for enterprise settlement (Source: Internal architecture illustration)

Stablecoins challenge this model by collapsing settlement into a single, shared digital layer. When used as stablecoin payment infrastructure, they function as a neutral settlement asset that moves value and finality together. Once a transaction is confirmed on-chain, settlement is complete. There is no separate clearing window and no delayed finality.

This is not a theoretical advantage. Large financial institutions are already treating tokenized money as infrastructure. JPMorgan Onyx has processed billions of dollars in tokenized payments through its internal blockchain networks, demonstrating how on-chain settlement can reduce intraday liquidity needs and operational friction. Similarly, global payment networks like Visa have publicly tested stablecoin settlement to move funds between institutions outside traditional banking hours.

The implication for enterprises is structural. When settlement becomes programmable, payments stop being a standalone product feature and start behaving like infrastructure. They can be triggered automatically by business events such as invoice approval, goods delivery confirmation, or treasury rebalancing. This aligns closely with how modern enterprises think about financial infrastructure: event-driven, auditable, and tightly integrated with operational systems.

Crucially, this shift also changes how value is measured. Instead of asking whether a stablecoin payment is cheaper or faster than SWIFT, enterprises evaluate whether it reduces reconciliation overhead, improves liquidity visibility, and shortens the time between economic activity and financial finality. Those outcomes sit squarely at the infrastructure level, not the product layer.

Enterprise and cross-border payments at scale

The strongest case for stablecoin payment infrastructure emerges in enterprise and cross-border payments, where legacy systems struggle the most. Multinational companies routinely manage dozens of bank accounts across regions to support payroll, suppliers, and intercompany transfers. Each account introduces trapped liquidity, FX exposure, and reconciliation complexity. At scale, enterprise payments are less about initiating transactions and more about how settlement, liquidity, and reconciliation are orchestrated.

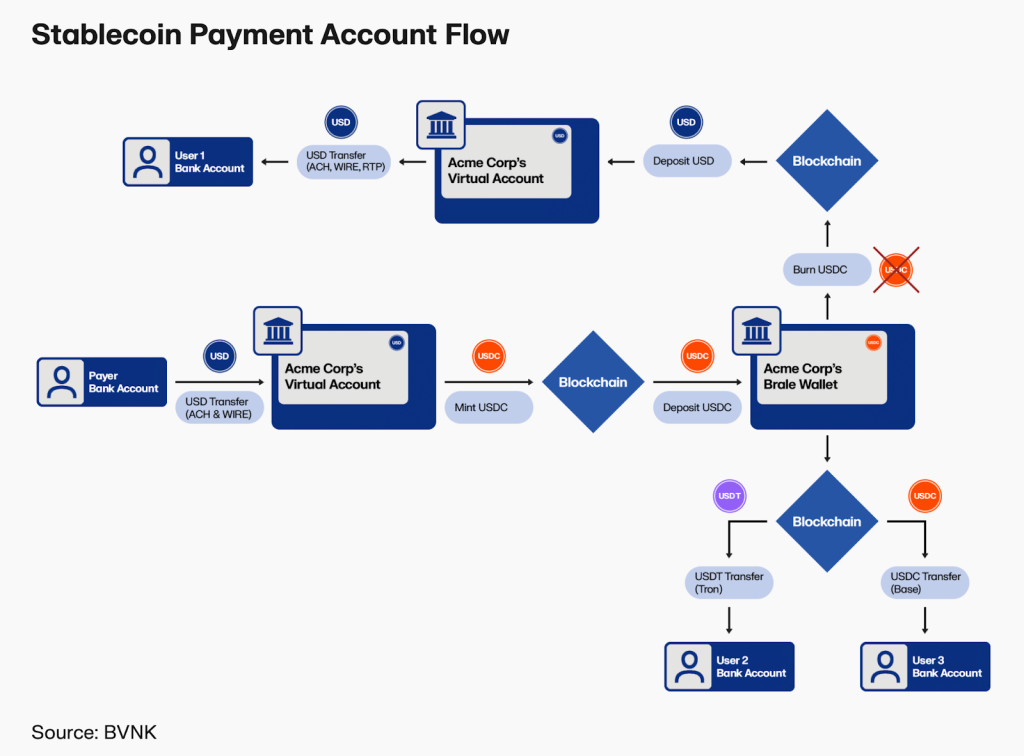

Enterprise stablecoin payment flow for cross-border settlement (Source: BVNK)

A stablecoin-based settlement layer offers a different architecture. Funds can be held in a unified on-chain treasury and deployed globally without routing through multiple correspondent banks. Cross-border payments become balance transfers on a shared ledger, with FX handled either through on-chain liquidity pools or regulated off-ramps. Settlement occurs in minutes rather than days, and liquidity can be reused immediately.

Data increasingly supports this shift. Industry analyses show that global cross-border payment costs remain stubbornly high, often exceeding 5 percent for certain corridors, while settlement times can extend beyond two business days. Stablecoin rails have demonstrated near-instant settlement with predictable fees, which materially alters cash flow dynamics for enterprises operating at scale.

However, treating stablecoins as infrastructure rather than a feature requires discipline. Enterprises cannot simply add a stablecoin payment option to an existing checkout flow and expect transformation. The real leverage appears when stablecoins are embedded deeper into financial workflows. This includes automated settlement tied to ERP events, real-time treasury visibility, and policy-driven controls over who can move funds and under what conditions.

This is where the notion of financial infrastructure becomes critical. Infrastructure must be boring, reliable, and defensible. It must survive audits, regulatory reviews, and internal risk assessments. Stablecoin systems designed for enterprises therefore need clear transaction traceability, role-based approvals, and alignment with accounting standards. Without these elements, stablecoins remain a tactical tool rather than a strategic layer.

Designing stablecoin payment infrastructure for ERP and compliance

Building stablecoin payment infrastructure that enterprises can trust requires more than blockchain expertise. It demands an understanding of how financial operations actually run. Payments do not exist in isolation. They are tightly coupled with ERP systems, accounting rules, and compliance processes that govern how money moves and how decisions are documented.

A production-grade stablecoin payment flow typically begins inside the ERP. An invoice is approved, a supplier payment is triggered, or an intercompany transfer is authorized. That business event initiates a payment instruction, which is translated into an on-chain transaction using stablecoins as the settlement asset. Once confirmed, the transaction status is written back to the ERP and accounting systems, closing the loop for reconciliation and reporting.

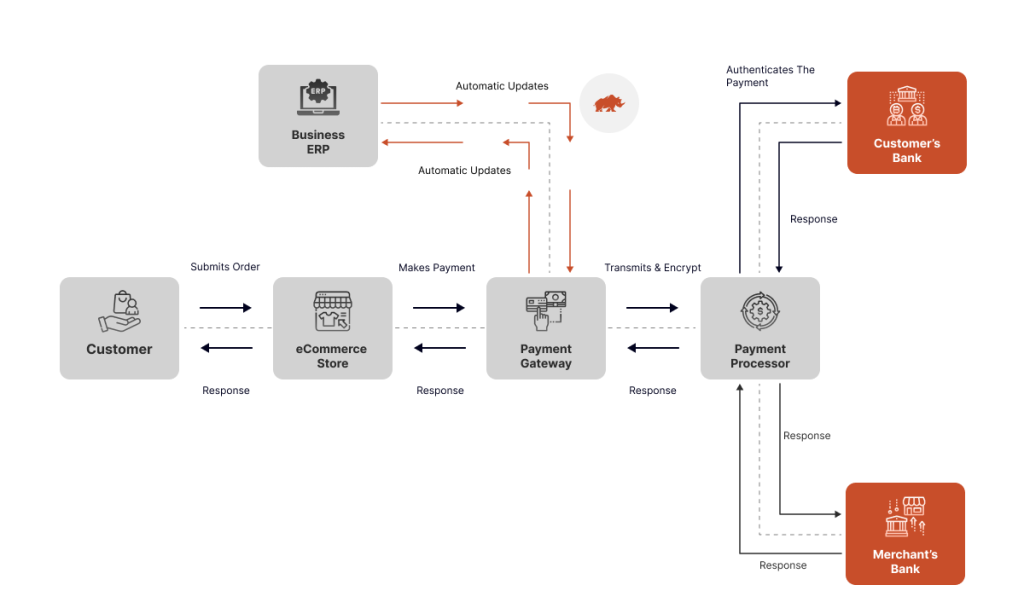

ERP-driven payment flow with settlement and banking integration (source: dckap)

This design has two strategic advantages. First, it preserves existing financial controls. Finance teams continue to operate within familiar approval workflows and audit trails. Second, it allows stablecoins to function as a settlement layer without disrupting upstream business logic. From the perspective of operations, the payment is still governed by ERP rules. The difference lies in how settlement is executed.

Compliance is equally central. Enterprises operate under a growing web of regulations related to AML, sanctions screening, and transaction monitoring. A viable stablecoin infrastructure must integrate these controls directly into the payment flow. This includes address screening, transaction limits, and real-time monitoring tied to compliance policies. Stablecoins issued by regulated entities, such as Circle’s USDC, are increasingly favored in these architectures because they offer clearer compliance assurances and institutional-grade transparency.

This is the layer where Twendee Lab operates most actively. Rather than positioning stablecoins as a front-end feature, Twendee designs them as part of the underlying financial infrastructure. Stablecoin payment flows are integrated directly with ERP and accounting systems, ensuring that settlement, reconciliation, and reporting remain coherent. Compliance requirements are embedded into the workflow itself, reducing operational risk while preserving the efficiency gains of on-chain settlement.

The result is not a crypto experiment, but a financial infrastructure upgrade. Stablecoins become invisible plumbing that supports enterprise payments, cross-border operations, and treasury management with greater speed and clarity.

Conclusion

Stablecoins are no longer competing with payment products. They are quietly redefining the settlement layer that enterprise payments depend on. As stablecoin payment infrastructure, they offer a path toward faster settlement, unified liquidity, and tighter integration with financial systems that enterprises already trust. The strategic opportunity lies not in adding stablecoins as a feature, but in designing them as infrastructure that aligns with ERP workflows, accounting logic, and compliance obligations.

For organizations navigating this transition, building on a thoughtfully designed settlement layer is increasingly becoming a prerequisite for modern enterprise payments. This is precisely the layer where Twendee Lab supports enterprises, by designing and integrating stablecoin-based payment infrastructure that fits existing ERP, finance, and compliance environments rather than disrupting them.